Blog

What Is Under and Over Invoicing ?

A Complete, Practical, and Global Trade Guide (2026 Edition)

Introduction: Why Under Invoicing and Over Invoicing Matter in International Trade

In international trade, the invoice is more than a document — it is the backbone of customs valuation, taxation, foreign exchange reporting, and risk management.

Two of the most misunderstood yet widely practiced mechanisms in global trade are:

Under Invoicing

Over Invoicing

These practices directly affect:

Customs duties and taxes

Capital flows and foreign exchange

Trade compliance and sanctions exposure

Corporate profitability and risk

National economic statistics

Under and Over invoicing

Despite being often associated with illegality, under invoicing and over invoicing exist on a wide spectrum, ranging from clearly illegal fraud to gray-area practices shaped by currency controls, sanctions, inflation, and capital restrictions.

This guide explains what they are, how they work, why they exist, and how they impact traders, governments, and economies worldwide.

What Is an Invoice in International Trade?

Before defining under or over invoicing, it is essential to understand the role of an invoice.

commercial invoice

A commercial invoice is a legally binding document that includes:

Description of goods

Quantity and unit price

Total value

Currency

Seller and buyer information

Incoterms

Country of origin

This invoice is used by:

Customs authorities

Tax authorities

Banks

Insurance companies

Regulators

Any manipulation of the invoice value therefore has direct legal, financial, and regulatory consequences.

Definition: What Is Under Invoicing?

Under Invoicing

Basic Definition

Under invoicing is the practice of declaring a value for goods on an invoice that is lower than the actual transaction value.

In simple terms:

The goods are worth more than what is written on the invoice.

Example (Simple)

Real value of goods: USD 100,000

Declared invoice value: USD 60,000

➡️ The invoice is under invoiced by USD 40,000

Why Under Invoicing Happens

Common motivations include:

Reducing customs duties

Avoiding VAT or sales tax

Capital flight

Currency control evasion

Sanctions circumvention

Informal profit retention

Under invoicing is extremely common in developing economies, sanctioned countries, and markets with high import tariffs.

Definition: What Is Over Invoicing?

Over Invoicing

Basic Definition

Over invoicing is the practice of declaring a value for goods on an invoice that is higher than the actual transaction value.

In simple terms:

The invoice shows more value than the goods are actually worth.

Example (Simple)

Real value of goods: USD 50,000

Declared invoice value: USD 90,000

➡️ The invoice is over invoiced by USD 40,000

Why Over Invoicing Happens

Common motivations include:

Moving capital out of a country

Accessing foreign currency

Money laundering

Tax planning (in some structures)

Artificially inflating costs

Sanctions-related financial routing

Under Invoicing vs Over Invoicing (Quick Comparison)

| Aspect | Under Invoicing | Over Invoicing |

|---|---|---|

| Declared value | Lower than real value | Higher than real value |

| Main motivation | Reduce duties / hide income | Capital movement / FX access |

| Customs impact | Lower tax paid | Higher declared import cost |

| Risk exposure | Customs fraud | AML & FX violations |

| Common regions | High-tariff countries | Currency-restricted countries |

Historical Background: Why These Practices Emerged

1. Colonial and Post-Colonial Trade Systems

Many developing countries inherited rigid customs systems with high tariffs designed for revenue extraction.

This created incentives for:

Smuggling

Under invoicing

Informal trade networks

2. Currency Controls and Capital Restrictions

Countries with:

Fixed exchange rates

Limited access to USD/EUR

Capital repatriation bans

Often unintentionally encourage over invoicing as a mechanism to move money across borders.

3. Sanctions and Trade Restrictions

Sanctioned countries frequently rely on:

Complex invoicing structures

Third-country intermediaries

Dual pricing mechanisms

These environments normalize invoice manipulation as a survival tool rather than a criminal exception.

Legal vs Illegal: The Gray Zone Most Traders Live In

Not all invoice adjustments are equally illegal.

Clearly Illegal:

Fake invoices

Phantom shipments

Double invoicing with intent to deceive authorities

Gray Area:

Transfer pricing adjustments

Dual contracts (commercial vs financial)

Service fee inflation

Licensing or IP cost reallocation

Legal (Under Strict Conditions):

Transfer pricing aligned with OECD rules

Adjustments documented and disclosed

Arm’s length pricing compliance

Economic Impact of Under and Over Invoicing

On Governments:

Loss of tax revenue

Distorted trade statistics

Weak currency reserves

On Companies:

Short-term profit gains

Long-term legal and reputational risk

Banking restrictions

On Economies:

Capital flight

Informal economy expansion

Reduced investor confidence

Why This Topic Matters More in 2026

In 2026, under and over invoicing are under unprecedented scrutiny due to:

AI-powered customs valuation systems

Data sharing between countries

AML and KYC expansion

Sanctions enforcement

OECD BEPS frameworks

At the same time, economic pressure, inflation, and geopolitical fragmentation continue to incentivize these practices.

How Trade Misinvoicing Works in Practice (With Real-World Structures)

Misinvoicing

1. Trade Misinvoicing: The Umbrella Concept

Before separating under invoicing and over invoicing operationally, it’s important to understand the broader concept:

What Is Trade Misinvoicing?

Trade misinvoicing refers to the deliberate falsification of the value, quantity, or nature of goods or services in cross-border trade documentation.

It includes:

Under invoicing

Over invoicing

Misclassification of goods

Phantom shipments

Double invoicing

According to global economic studies, trade misinvoicing accounts for hundreds of billions of USD annually in illicit financial flows.

2. How Under Invoicing Works in Real Trade Scenarios

2.1 The Basic Commercial Structure

In a standard export/import transaction:

Seller issues an invoice

Buyer pays based on invoice value

Customs duties and taxes are calculated from the invoice

Under invoicing occurs when the declared invoice does not reflect the real commercial value.

2.2 Typical Under Invoicing Structures (High-Level)

Below are commonly observed patterns, described for understanding and compliance awareness:

Structure A: Partial Invoice Declaration

One invoice is presented to customs

The remaining value is settled outside official banking channels

Risk exposure:

Customs fraud, tax evasion, AML flags

Structure B: Dual Pricing (Commercial vs Financial)

Commercial agreement reflects true value

Financial invoice reflects lower value

Often seen in:

High-tariff countries, import-restricted markets

Structure C: Misclassification + Undervaluation

Goods declared as a lower-value HS code

Value reduced accordingly

Example:

Industrial equipment declared as spare parts

2.3 Industries Where Under Invoicing Is Most Common

| Industry | Reason |

|---|---|

| Textiles & apparel | High tariffs, price variability |

| Electronics | Fast depreciation, valuation ambiguity |

| Automotive parts | Complex HS codes |

| Construction materials | Bulk pricing opacity |

| Consumer goods | Price dispersion by market |

3. How Over Invoicing Works in Real Trade Scenarios

3.1 Core Logic of Over Invoicing

Over invoicing reverses the mechanism:

Declared value exceeds real value

Excess value is used to justify cross-border fund movement

This is often linked to foreign exchange access or capital controls.

3.2 Common Over Invoicing Structures (High-Level)

Structure A: Inflated Import Invoice

Goods priced above market value

Excess payment retained abroad

Common in:

Currency-restricted economies

Structure B: Related-Party Overpricing

Importing from an affiliated company

Prices manipulated through transfer pricing abuse

Triggers:

OECD BEPS scrutiny, tax audits

Structure C: Service & Intangible Inflation

Instead of goods:

Management fees

Licensing fees

Technical services

These are easier to inflate due to valuation subjectivity.

3.3 Industries Where Over Invoicing Is Common

| Sector | Reason |

|---|---|

| Machinery & equipment | Custom pricing |

| Oil & gas services | Intangible costs |

| Pharmaceuticals | IP licensing |

| Software & IT | Non-physical valuation |

| Consulting & engineering | Subjective pricing |

4. Under Invoicing vs Over Invoicing: Behavioral Differences

| Dimension | Under Invoicing | Over Invoicing |

|---|---|---|

| Objective | Reduce payable amounts | Move capital / access FX |

| Customs role | Central risk | Secondary role |

| Banking role | Limited | High AML scrutiny |

| Detection method | Price comparison | FX monitoring |

| Typical counterpart | Buyer-driven | Seller-driven |

5. Real-World Country Patterns (Macro-Level)

5.1 Emerging Markets

High tariffs

Weak enforcement

➡️ Under invoicing dominant

5.2 Currency-Controlled Economies

FX shortages

Capital exit restrictions

➡️ Over invoicing dominant

5.3 Sanctioned or Semi-Sanctioned States

Restricted banking

Third-country routing

➡️ Both practices coexist

6. Customs Valuation: Why Authorities Care

Customs authorities rely on:

WTO Customs Valuation Agreement

Transaction value principle

Comparable pricing databases

AI risk engines

Red Flags Customs Monitor:

Prices far below reference values

Repeated identical pricing across shipments

Mismatch with weight or specification

Related-party transactions

7. Banking & AML Perspective

Banks increasingly cross-check:

Invoice value vs market benchmarks

Trade route plausibility

Payment-to-goods ratio

Repeated abnormal margins

Key point:

Many trade misinvoicing cases are detected by banks, not customs.

8. The Compliance Reality for Traders

Many companies unintentionally expose themselves by:

Accepting supplier invoices without validation

Using outdated price references

Poor transfer pricing documentation

Weak internal trade controls

This is why professional trade compliance advisory is now a competitive necessity.

9. Why Professional Consultation Matters

In complex markets:

Valuation disputes are common

Regulations change rapidly

Enforcement is inconsistent

👉 For consultation on compliant international trade structures, risk assessment, and sourcing strategies — especially in high-risk markets — businesses are strongly advised to work with experienced trade and compliance consultants.

OPERATIONAL MECHANICS, DETECTION, AND THE 2026 LANDSCAPE

10. The Financial Flows: How Money Moves in Misinvoicing Schemes

Understanding the monetary flow is crucial to grasping the full picture. The invoice is just one document; the payment trail often tells the real story.

10.1 Payment Mechanisms in Under Invoicing

The core challenge: How does the buyer pay the seller the undeclared balance?

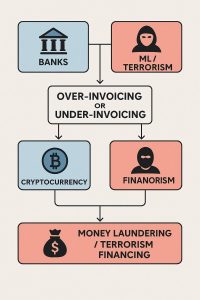

The Informal Settlement (Hawala/Underground Banking): The buyer pays the balance via informal value transfer systems, often in local currency within the seller’s country. This leaves no international paper trail.

Offsetting Through Other Transactions: The balance is settled through a separate, seemingly unrelated transaction (e.g., a consulting fee, a dividend payment, or a loan repayment).

Future Credit: The balance is treated as an informal credit against future trade, creating a complex web of mutual obligations.

Physical Transfer of Value: In extreme cases, value is transferred via physical assets (e.g., gold, gems) or other commodities.

10.2 Payment Mechanisms in Over Invoicing

Here, the challenge is justifying the outward flow of excess funds.

Direct Bank Transfer: The most straightforward method. The buyer’s bank transfers the full inflated amount to the seller, relying on weak banking AML checks or complicit trade finance officers.

Loans and Advances: The excess is disguised as an advance payment for future goods or a loan to the overseas seller, which is never repaid.

Intercompany Accounts: In multinational corporations, the excess is buried in complex intercompany account settlements, often over multiple quarters.

11. The Role of Intermediaries and Trade Hubs

Pure direct buyer-seller misinvoicing is risky. Sophisticated operations use intermediaries.

Third-Country Reinvoicing Centers: A company in a low-regulation jurisdiction (e.g., a Dubai or Hong Kong-based trading company) acts as the official buyer from the supplier and the official seller to the end buyer. They issue two different invoices, facilitating the value manipulation with a layer of legal separation.

Free Trade Zones (FTZs): FTZs, with their lax oversight and duty-free status, are often used to reroute goods, alter documentation, and repackage shipments to obscure origin and true value before final shipment to the destination country.

Falsified Origin and Transit Documents: Goods are routed through multiple countries, with documentation altered at each transit point to gradually build a “legitimate” but false paper trail supporting the misdeclared value.

12. Detection and Prevention: The Government and Institutional Arsenal (2026 Update)

By 2026, the tools available to authorities are more integrated and intelligent than ever.

12.1 Customs Modernization & AI Valuation

Global Price Reference Databases: Customs authorities no longer rely on sporadic checks. They maintain real-time, commodity-specific global price databases fed by thousands of actual transactions, UN Comtrade data, and market intelligence platforms. Declared values are instantly benchmarked.

Predictive Risk Engines: AI algorithms analyze thousands of data points per shipment: historical patterns of the importer/exporter, country of origin/route, vessel tracking, financial data of involved parties, and even news about market price fluctuations. Shipments are assigned a risk score, dictating the level of inspection.

Non-Intrusive Inspection (NII): Advanced X-ray, gamma-ray, and spectroscopic scanners at ports can verify declared contents against manifests, detecting weight, density, and material anomalies that suggest misdeclaration.

12.2 Financial Sector Surveillance

Trade-Based Money Laundering (TBML) Red Flags: Banks have standardized TBML detection indicators. These include:

Mismatched Goods & Payment: Payment from a sector unrelated to the shipped goods.

Round-Tripping: Rapid succession of imports and exports between the same parties with inflated values.

Use of High-Risk Jurisdictions: Transactions funneled through jurisdictions known for weak oversight.

Over- or Under-Use of Trade Finance: Unnecessary use of complex letters of credit for simple trades, or conversely, avoidance of all banking instruments.

The SWIFT ICP Effect: The wider adoption of ISO 20022 messaging standards and increased data sharing between banks and customs authorities creates a more transparent payment-versus-goods ecosystem.

12.3 International Data Sharing Initiatives

BEPS 2.0 & Country-by-Country Reporting (CbCR): The OECD’s Base Erosion and Profit Shifting project forces multinationals to report revenue, profit, and taxes paid in every jurisdiction. Discrepancies in intercompany pricing (a form of over/under invoicing) are flagged for audit.

Automatic Exchange of Information (AEOI): Tax authorities globally automatically share financial account information, making it harder to hide the proceeds of misinvoicing in offshore bank accounts.

Joint Customs & Tax Audit Teams: Many countries have broken down silos, creating task forces where customs, tax, and financial intelligence units work together on major cases.

13. Regional Deep Dives: How Misinvoicing Manifests Across the Globe

13.1 Asia: The Manufacturing Hub Complexities

China & Vietnam: Predominantly under invoicing risks from exporting hubs, driven by buyers in high-tariff countries seeking to lower duties. Authorities combat this with export declaration minimum prices for certain goods.

India & Indonesia: A mix of under invoicing for luxury and electronic imports to avoid high duties, and over invoicing for capital goods imports as a means of capital flight. Strict foreign exchange (forex) controls in India (e.g., the Liberalized Remittance Scheme limits) create incentives for over invoicing imports to move more capital out.

Singapore & Hong Kong: As major trading hubs, they are often used as reinvoicing centers. Their strong legal frameworks are leveraged against illegal activities, but the volume of trade makes monitoring every transaction challenging.

13.2 Africa: The Informality and Currency Challenge

High-Tariff Nations (e.g., Nigeria, Angola): Rampant under invoicing of imports to evade duties that can exceed 50% of value. This is exacerbated by widespread informal trade networks.

Currency-Depressed Economies (e.g., Zimbabwe, Malawi): Over invoicing of imports is a primary method for moving hard currency out of the country and accessing USD outside official, overvalued exchange rates.

Extractive Industries: A global hotspot for misinvoicing. Under invoicing of mineral exports (gold, diamonds, cobalt) from source countries, and over invoicing of equipment imports by mining companies, lead to massive revenue losses for governments.

13.3 The Americas: Sanctions and Proximity

Venezuela & Cuba: Case studies in sanctions-driven misinvoicing. Complex routing through third countries, dual documentation, and the use of cryptocurrencies to settle balances have become normalized.

Mexico & Latin America: Significant under invoicing of consumer goods imports from Asia and the US, motivated by high VAT and import tariffs. Also, over invoicing related to drug trade money laundering, using imports of high-value, hard-to-verify goods (e.g., precious stones, artwork, electronics).

13.4 Europe & Developed Economies: The Sophisticated Avoidance

EU Single Market: Less focus on customs duty evasion between member states, but significant focus on VAT carousel fraud (a form of misinvoicing linked to missing trader intra-community fraud). Also, over invoicing by companies importing from low-tax jurisdictions within corporate groups to shift profits.

United States: Focus is heavily on sanctions evasion (e.g., Russia, Iran), anti-dumping duty circumvention (e.g., steel, aluminum), and intellectual property royalty mispricing. The Bureau of Industry and Security (BIS) and OFAC play a major role alongside Customs and Border Protection (CBP).

14. Strategic Implications for Businesses in 2026

In this tightened enforcement environment, companies must move from a reactive to a proactive stance.

14.1 Building a Defensible Trade Compliance Program

Robust Internal Controls: Implement a clear, documented process for verifying and documenting the valuation of imported/exported goods. This includes obtaining and filing supporting documents like manufacturer price lists, third-party valuation reports, and royalty/licensing agreements.

Transfer Pricing Master File & Local File: For multinationals, having OECD-aligned, contemporaneous transfer pricing documentation is no longer optional—it’s a primary defense during audits.

Regular Risk Assessments: Conduct periodic reviews of trade partners, product categories, and countries involved in the supply chain for misinvoicing risks.

Employee Training: Ensure staff in procurement, logistics, and finance understand red flags and the severe consequences of complicity.

14.2 Technology as a Shield

Global Trade Management (GTM) Software: Use GTM systems that integrate with customs databases, denied party lists, and provide HS code classification and valuation support.

Blockchain Pilots: While not yet universal, participating in blockchain-based trade platforms (like TradeLens or we.trade) can provide an immutable, shared record of transactions, reducing the opportunity for document manipulation.

Data Analytics: Use internal data analytics to monitor your own trade patterns for anomalies that could indicate unintentional errors or internal fraud.

15. The Future of Trade Misinvoicing (2026 and Beyond)

The cat-and-mouse game will evolve. As authorities get smarter, so will the methods.

15.1 Emerging Evasion Techniques

Cryptocurrency and CBDC Settlements: Using cryptocurrencies or future Central Bank Digital Currencies (CBDCs) to settle invoice differentials offers greater anonymity and cross-border fluidity.

Manipulation of “Low-Value” Shipments: With the global rise in de minimis thresholds (e.g., the US’s $800 limit), misdeclaring high-value goods as multiple low-value parcels to avoid scrutiny and duties is a growing trend.

Exploiting E-Commerce Complexity: The sheer volume of small e-commerce parcels makes manual inspection impossible, creating a new frontier for misdeclaration of value and description.

15.2 The Countervailing Forces of Enforcement

AI and Machine Learning Dominance: Detection algorithms will move from rules-based to predictive, learning from new patterns in real-time.

Global Carbon Tax and Border Adjustments: As carbon border adjustment mechanisms (CBAM) are implemented, misdeclaring the carbon intensity or value of goods to evade these new levies will become a new battleground.

Unified International Enforcement: Increased political will, especially from the G7 and G20, to combat illicit financial flows will drive more joint operations and sanctions against enablers (banks, logistics firms, trading companies).

Conclusion: Navigating the New Reality

Under invoicing and over invoicing are not relics of a less regulated past. They are dynamic practices shaped by the fundamental pressures of global economics: tariff disparities, currency imbalances, capital restrictions, and geopolitical conflict.

The 2026 landscape presents a paradox: the tools for detection are more powerful than ever, yet the economic incentives to engage in trade misinvoicing remain strong, and in some cases, have intensified.

For legitimate businesses, this means that compliant trade operations are a strategic imperative, not a back-office function. The cost of getting it wrong has escalated from a customs penalty to include bank de-risking (loss of accounts), reputational catastrophe, and even criminal liability for executives.

The path forward requires:

Acknowledgment: Accepting that these practices exist in your supply chain’s regions and among potential partners.

Vigilance: Implementing the people, processes, and technology to protect your organization from both intentional wrongdoing and unintentional error.

Expertise: Recognizing that global trade compliance is a specialized field. Building internal competence and, where necessary, engaging with experienced trade compliance consultants, legal advisors, and customs specialists is not an expense—it is critical risk management and a foundation for sustainable international growth.

In the end, the commercial invoice remains the backbone of international trade. Ensuring its integrity is the surest way to build a resilient, profitable, and defensible global business in 2026 and beyond.