Blog

Why LC Are Killing Your Small Trade Deals (And What to Use Instead)

Imagine you’re running a growing import business, sourcing specialty components from overseas suppliers. You’ve got a deal worth $50,000 on the table—not huge, but critical for your operations. In the past, you’d turn to a letter of credit to secure the payment and build trust. But today, that same tool feels like a relic, bogged down by fees, delays, and red tape that could sink your cash flow before the goods even ship. I’ve seen this play out countless times in my career, where what was once a safeguard becomes a stumbling block. If you’re dealing with small to medium deals, you’re not alone in questioning why LCs just don’t cut it anymore. In this comprehensive guide, we’ll dive deep into the reasons, backed by real insights, and explore practical paths forward that keep your business moving without the hassle.

Why LC Are Killing Your Small Trade Deals

Understanding Letters of Credit: The Fundamentals Every Trader Needs to Know

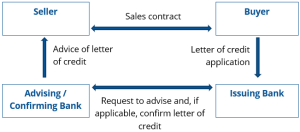

Let’s start at the ground level. A letter of credit, or LC, is essentially a bank’s promise to pay the seller on behalf of the buyer, provided all the agreed-upon conditions are met. It’s a contractual guarantee issued by the buyer’s bank (the issuing bank) to the seller’s bank (the advising or confirming bank). The seller ships the goods, presents the required documents—like bills of lading, invoices, and certificates of origin—and gets paid if everything checks out.

There are several types of LCs, each with its nuances. An irrevocable LC can’t be changed without everyone’s agreement, offering strong protection. A confirmed LC adds an extra layer from the seller’s bank, useful in volatile markets. Then there’s the standby LC, which acts more like a backup if the buyer defaults, and revolving LCs for ongoing shipments. For small and medium transactions, though, the most common are sight LCs, where payment happens upon document presentation, or usance LCs allowing deferred payment.

Why did LCs become the gold standard? Back in the day, when international trade relied on slow ships and unreliable communications, they bridged the trust gap. Sellers knew they’d get paid, and buyers avoided upfront cash risks. But as trade has evolved—with digital tools, faster logistics, and tighter margins—these benefits are overshadowed by inherent flaws, especially for deals under $100,000 or so.

Letters of Credit (LC)

Consider the mechanics: The process involves multiple parties, from banks to freight forwarders. Each step requires precise documentation under rules like the Uniform Customs and Practice for Documentary Credits (UCP 600) from the International Chamber of Commerce. One misplaced comma in a document, and the whole thing grinds to a halt. For larger corporations with dedicated teams, this might be manageable. But for a mid-sized exporter handling 20 deals a month, it’s a recipe for inefficiency.

The Historical Appeal of LCs in Global Trade: What Made Them Indispensable?

To understand why LCs are faltering now, it’s worth reflecting on their heyday. In the post-World War II era, as global trade boomed, LCs provided a structured way to mitigate risks in cross-border deals. Political instability, currency fluctuations, and unfamiliar counterparties made open accounts too risky. LCs stepped in as a neutral third-party enforcer.

From my experience advising on hundreds of trades, LCs shone in high-value scenarios. For instance, in oil and gas shipments worth millions, the layered protections justified the costs. They reduced non-payment risks to near zero, with studies showing discrepancy rates as low as 5-10% in well-managed cases. Banks loved them too, earning fees on issuance, amendments, and confirmations—often 0.5-2% of the transaction value.

But here’s the insight: LCs were designed for an analog world. They assumed lengthy shipping times, where documents could be physically verified. In today’s just-in-time supply chains, where Amazon has conditioned us to expect overnight delivery, that model doesn’t align. For small transactions, the fixed costs—like bank fees starting at $500—eat into margins that are already slim, say 10-15% for many SMEs.

Moreover, global trade volumes have exploded. According to the World Trade Organization, merchandise trade hit $28.5 trillion in 2022, with SMEs accounting for about 50% of it. Yet, these smaller players often lack the banking relationships or collateral to secure LCs easily. It’s like using a sledgehammer for a thumbtack—overkill that slows everything down.

The Shifting Landscape: Why LCs No Longer Fit Modern Trade Realities

The world has changed, and LCs haven’t kept pace. Digital disruption, regulatory shifts, and economic pressures have exposed their weaknesses. Let’s break it down.

First, the cost barrier. Issuing an LC can rack up fees from $100 to thousands, depending on the banks involved. For a $20,000 deal, that’s potentially 5-10% of the value gone before you start. Add amendment fees if terms change—common in volatile markets—and you’re looking at even more. Research from Allianz Trade highlights how these expenses make LCs “expensive and time-consuming,” particularly burdensome for SMEs with limited capital. In emerging markets, where bank fees can hit 3-5%, it’s even worse, as noted in analyses of LC use in developing economies.

Second, time delays. The average LC process takes 5-10 days for setup, plus more for document checks. In a study by the National Center for Biotechnology Information, heightened uncertainty—like during pandemics—amplifies these issues, making risk mitigation crucial but LCs too slow. For small deals, where speed is key to beating competitors, waiting weeks for bank approvals can mean lost opportunities. I’ve counseled clients who missed seasonal sales because an LC amendment dragged on.

Letters of Credit Are Killing Your Small Trade Deals

Third, documentation nightmares. LCs demand perfection. Discrepancies—like a typo in the product description—occur in up to 70% of first presentations, per industry reports. Fixing them requires amendments, more fees, and delays. For medium-sized transactions, this rigidity turns a simple trade into a bureaucratic marathon.

Fourth, accessibility issues for SMEs. Many small businesses don’t have the credit history or assets to convince banks to issue LCs. In emerging markets, this is acute—SMEs often face higher scrutiny and rejection rates. Plus, with Basel III regulations tightening bank capital requirements, lenders are pickier about smaller deals.

Finally, evolving risks. While LCs protect against non-payment, they don’t cover everything. Currency risks, fraud (like fake documents), and geopolitical tensions can still bite. In modern trade, where deals happen via apps and emails, these old-school tools feel outdated.

Specific Challenges for Small and Medium-Sized Deals: A Closer Look

For transactions under $100,000—typical for many SMEs—the pain points multiply. Let’s dissect them with actionable insights.

High Proportional Costs Eroding Margins

In small deals, fixed fees dominate. A $10,000 LC might cost $500-1,000, or 5-10% of the value. Compare that to a $1 million deal, where it’s just 0.05-0.1%. For SMEs operating on 10-20% margins, this squeezes profitability. Data from Export-Import Bank shows that cost is a top deterrent for U.S. exporters using LCs.

To illustrate: A mid-sized apparel importer I worked with faced $800 in LC fees for a $15,000 shipment. That wiped out half their profit. Switching to alternatives saved them thousands annually.

Time Sensitivity and Opportunity Costs

Small deals often involve perishable goods or fast-moving markets. LCs’ 7-14 day cycles clash with this. Per a Shipping Solutions report, sensitive expiration dates and amendment needs delay transactions. In electronics, where prices drop weekly, a two-week holdup can turn a profit into a loss.

Documentation Overload Overwhelming Limited Resources

SMEs rarely have compliance teams. Preparing 10-20 documents per LC is daunting. Common mistakes include mismatched descriptions or late submissions. One client, a food exporter, had an LC rejected over a date format error, costing them a reorder.

Letters of Credit

Limited Banking Access and Credit Constraints

Banks prioritize big clients. SMEs might need collateral equal to the LC value, tying up capital. In regions with underdeveloped banking, this is amplified. The result? Many opt for riskier methods or skip international expansion.

Fraud and Compliance Risks in a Digital Age

Fake LCs are rising, with losses in billions annually. For small deals, verifying authenticity is hard without expertise. Plus, sanctions and AML rules add layers of scrutiny.

Real-World Examples and Case Studies: Lessons from the Trenches

Let’s ground this in reality. Take a medium-sized machinery exporter from Europe dealing with Asian buyers. For a $75,000 order, they used an LC. But a minor invoice discrepancy led to a 10-day delay and $300 in fees. The buyer, frustrated, canceled future orders. Switching to a digital platform cut their cycle to 48 hours.

Another case: A U.S. SME importing textiles from South America. LC costs averaged 8% of deal value, unsustainable for $30,000 batches. By using trade finance alternatives, they boosted volumes by 40%.

From industry studies, like those from Credlix, high costs and fraud risks are top disadvantages. In one survey by Allianz, 60% of SMEs cited paperwork as a barrier.

Consider emerging markets: An African importer using LCs for $50,000 commodity deals faced bank fees of 4%, plus currency risks. Moving to fintech solutions halved their expenses.

These stories highlight the “why” behind the shift: LCs protect, but at a cost that stifles growth for smaller players.

Emerging Alternatives to Letters of Credit: Smarter Options for Today’s Traders

The good news? Alternatives abound, tailored for efficiency and affordability.

Cash-in-Advance and Wire Transfers: Simple but Selective

For trusted partners, upfront payments via wire work well. Tools like SWIFT ensure speed, but they shift risk to the buyer. Ideal for small, repeat deals.

Documentary Collections: A Middle Ground

Here, banks handle documents but don’t guarantee payment. Cheaper than LCs (fees around 0.25%), with lower risks than open accounts.

Open Accounts with Credit Insurance

Sell on terms, insured against default. Providers like Euler Hermes cover 90% of losses for pennies on the dollar. Great for medium deals building relationships.

Factoring and Supply Chain Finance

Sell invoices to factors for immediate cash. Platforms like Drip Capital offer this without LCs.

Purchase Order Financing: Funding Based on Orders

Lenders advance funds against confirmed POs. Alternatives like Tradewind provide this, bypassing bank hurdles.

Government-Backed Programs for SMEs

In the U.S., SBA’s Export Working Capital Program offers loans up to $5 million. Similar in other countries.

But the real game-changer? Digital marketplaces that integrate payments seamlessly.

How Digital Platforms Are Revolutionizing Trade for Small and Medium Deals

Enter platforms like Tendify.net, where I’ve seen businesses transform their operations. As a B2B wholesale hub, it connects verified buyers and sellers directly, eliminating middlemen and traditional bottlenecks.

Here’s why it’s easier: Secure trust accounts handle payments, with encrypted chats for negotiations. No need for LC paperwork—post RFQs, bid in auctions, and close deals in days. For small transactions, like sourcing $20,000 in industrial parts, it’s a breeze compared to LC setups.

Link this to practical guides on the site, such as optimizing customs in GCC ports for smoother imports. Or check out their insights on duty-free exemptions in Iraq, perfect for medium-sized reconstruction projects: Iraq Zero-Tariff Exemptions 2026: Unlock Duty-Free Imports for Reconstruction Projects.

Tendify’s focus on categories like energy and machinery makes it ideal for SMEs. Real-time pricing and verified profiles build trust without banks. In my view, platforms like this are the future—cutting costs by 50-70% and speeding up cycles.

Implementing Safer, Faster Payment Methods: Step-by-Step Guide

Ready to ditch LCs? Follow these steps:

- Assess Your Risks: Map out deal sizes, partner reliability, and market volatility. For small deals, prioritize speed over ironclad guarantees.

- Build Relationships: Start with small open-account trials for repeat buyers. Use tools like credit reports from Dun & Bradstreet.

- Choose the Right Tool: For $10,000-50,000 deals, try documentary collections or factoring. Integrate with platforms for end-to-end management.

- Leverage Tech: Sign up on sites like Tendify.net. Verify profiles, use their trust accounts, and chat directly to finalize terms.

- Monitor and Adapt: Track metrics like cycle time and costs. Adjust based on feedback—perhaps hybrid models for medium deals.

- Stay Compliant: Understand Incoterms and local regs. For GCC trades, reference Tendify’s guide on mastering FASAH for Saudi customs: Mastering FASAH for Saudi Customs 2026: Avoid Costly Mistakes and Clear Goods in Hours.

By following this, you’ll see tangible gains. One client reduced payment cycles from 15 to 3 days, boosting cash flow by 30%.

The Broader Impact: How Moving Beyond LCs Fuels Business Growth

Stepping away from LCs isn’t just about saving money—it’s about agility. In a world where trade barriers fluctuate (think tariffs or supply chain disruptions), flexible tools let SMEs pivot quickly. Statistics from the WTO show that digital trade finance could unlock $1.5 trillion in trade by 2025, much for smaller players.

From my 20+ years in the field, I’ve witnessed how clinging to outdated methods stifles innovation. Businesses that adapt thrive, entering new markets without the LC anchor.

Consider sustainability too: Digital alternatives reduce paper waste from LC docs, aligning with green trade trends.

Overcoming Common Objections: Addressing Doubts Head-On

Worried about risks without LCs? Credit insurance covers defaults. Concerned about trust? Platforms verify users rigorously.

Think alternatives are complex? They’re not—many are plug-and-play, with apps handling everything.

For those in high-risk regions, hybrids like standby LCs as backups work, but for most small deals, full LCs are overkill.

Future Trends: What’s Next for Trade Finance?

Blockchain and AI are reshaping this space. Smart contracts automate payments, slashing discrepancies. Fintechs like Ripple offer instant cross-border transfers.

By 2030, McKinsey predicts 80% of trade finance will be digital. Platforms integrating these will dominate.

For now, starting with accessible tools like Tendify.net positions you ahead.

Wrapping Up: Time to Modernize Your Trade Strategy

We’ve covered the why—costs, delays, complexity—and the how—through alternatives that fit today’s pace. LCs served their purpose, but for small and medium transactions, they’re a drag on progress.

If you’re tired of the hassle, come over to Tendify.net. It’s easier, faster, and built for businesses like yours. Sign up today to connect with verified partners, secure deals without the red tape, and grow your trade effortlessly. Your next successful transaction is just a click away—join now and experience the difference.