Blog

Green Technologies invesment in ASEAN

Investment Opportunities in Renewable Energy Across Southeast Asia

Southeast Asia stands at the threshold of one of the most significant energy transitions in the developing world. With a young and growing population, rapid urbanization, and rising energy demand, the ten ASEAN member states are increasingly turning toward renewable energy technologies to meet their future power needs in a sustainable and economically viable manner. Solar, wind, hydropower, biomass, and emerging green hydrogen solutions are no longer peripheral options — they are becoming central pillars of national energy strategies across the region.

Investment Opportunities in Renewable Energy

This comprehensive guide provides investors, project developers, technology providers, and compliance professionals with a clear, audit-ready analysis of renewable energy investment opportunities in ASEAN. It examines policy frameworks, market potential, technology trends, financing mechanisms, and practical considerations for compliant and responsible investment in one of the world’s fastest-growing clean energy regions.

Strategic Insight: ASEAN’s renewable energy transition is driven by a powerful combination of necessity and opportunity. Rising energy demand, falling technology costs, ambitious national targets, and increasing access to green finance are creating a fertile environment for long-term, high-impact investments that deliver both commercial returns and measurable environmental benefits.

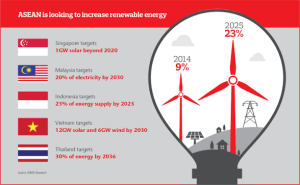

The ASEAN Energy Transition Context

ASEAN’s energy demand is projected to grow significantly in the coming decades as economies expand and millions more people gain access to modern energy services. At the same time, the region faces the dual challenge of ensuring energy security while addressing climate change commitments and local environmental concerns.

The ASEAN Energy Transition Context

Renewable energy offers a practical pathway to meet these challenges. Abundant solar resources across the archipelago, strong wind potential in coastal and mountainous areas, extensive hydropower capacity in the Mekong and other river basins, and growing interest in biomass and green hydrogen create a diverse renewable energy portfolio. National governments have responded with increasingly ambitious targets, policy incentives, and regulatory reforms designed to accelerate deployment.

For international investors and technology providers, ASEAN represents one of the most attractive renewable energy growth stories globally. The combination of policy support, improving grid infrastructure, and rising corporate demand for clean energy creates multiple entry points across the project development value chain. For companies seeking diversified and resilient supply chain strategies in Asia, renewable energy investment in ASEAN offers both commercial and sustainability benefits. Related supply chain considerations are explored in Vietnam: The New Factory of the World – Why Tech Giants Are Moving Production from China to Vietnam.

ASEAN Green Technologies Market Outlook 2026: Key Figures and Projections

ASEAN’s green technology sector is experiencing robust growth driven by policy support, falling technology costs, and rising corporate and investor demand for sustainable solutions. Key market indicators for 2026 include:

- Renewable energy investment in Southeast Asia is projected to continue its upward trajectory, with solar and wind leading deployment.

- Regional solar capacity additions remain strong, supported by competitive auction mechanisms and improving grid infrastructure.

- Green hydrogen is gaining policy attention as a long-term storage and industrial decarbonization solution, with several countries developing pilot projects and national strategies.

- Green logistics and sustainable supply chain solutions are expanding rapidly as multinational corporations and regional players seek to reduce Scope 3 emissions and comply with international ESG standards.

The combination of ambitious national renewable energy targets, increasing access to green finance, and corporate power purchase agreements (PPAs) is creating a favorable environment for both local and international participants. Investors and technology providers who adopt a long-term, compliance-focused approach are best positioned to capture value across the project lifecycle — from development and financing to operations and asset management.

Success in this market requires not only capital and technology but also deep understanding of local regulatory frameworks, environmental and social considerations, and grid integration challenges. Those who combine financial strength with technical expertise and strong local partnerships are likely to achieve sustainable competitive advantage in ASEAN’s evolving green economy.

Solar Energy: The Dominant Growth Engine

Solar power has emerged as the fastest-growing renewable energy source in ASEAN. Abundant sunshine across much of the region, rapidly declining panel costs, and supportive policies have made utility-scale solar, rooftop solar, and floating solar projects increasingly attractive.

Solar Energy

Countries such as Vietnam, Thailand, Indonesia, Malaysia, and the Philippines have made impressive progress in solar deployment. Vietnam, in particular, experienced one of the fastest solar capacity build-outs in recent years, demonstrating the region’s potential when policy frameworks align with investor interest. Floating solar projects on existing reservoirs and hydropower dams offer innovative solutions that minimize land use conflicts while providing additional benefits to existing infrastructure.

Investment opportunities span the full value chain: project development, EPC services, equipment supply, operations and maintenance, and green financing. For technical contractors and equipment suppliers, the solar boom creates sustained demand for high-quality components, inverters, mounting systems, and grid integration technologies. Strategic approaches to participating in regional energy infrastructure projects are detailed in Rebuilding Energy Infrastructure: Strategic Opportunities for Technical Contractors in Post-Ceasefire Reconstruction.

Wind Energy and Emerging Offshore Potential

While solar currently leads deployment, wind energy — both onshore and increasingly offshore — holds significant long-term potential. Coastal areas in Vietnam, the Philippines, Thailand, and Indonesia offer favorable wind resources, particularly for offshore development as technology costs continue to decline.

Asean Wind Energy

Several countries have introduced specific wind power policies, auction mechanisms, and grid connection frameworks to encourage investment. Offshore wind, though still in early stages in most ASEAN nations, is attracting growing interest from international developers with experience in Europe and other mature markets. The combination of improving policy clarity and technological maturity positions offshore wind as a major future growth area.

For investors, wind projects often require larger capital commitments but can deliver attractive long-term returns through power purchase agreements with state utilities or corporate off-takers. Compliance with local content requirements, environmental impact assessments, and grid integration standards remains essential for project success.

Hydropower, Biomass, and Green Hydrogen

Hydropower continues to play a significant role in several ASEAN countries, particularly those with extensive river systems. While large-scale projects face environmental and social considerations, smaller run-of-river and pumped-storage solutions are gaining attention for their ability to support grid stability as renewable penetration increases.

Hydropower, Biomass, and Green Hydrogen

Biomass and bioenergy projects utilizing agricultural residues, palm oil waste, and forestry by-products offer decentralized solutions that support rural development while contributing to energy security. Green hydrogen, though still in early development stages, is attracting policy interest as a potential long-term storage and industrial feedstock solution.

The diversification of renewable sources strengthens overall system resilience and creates multiple investment entry points across different technologies and project scales. For insight into how alternative fuels and green technologies are reducing logistics costs in major Asian markets, refer to Reducing Logistics Costs in India Through Alternative Fuels: The Role of Electric Vehicles and Green Hydrogen in Optimizing Domestic Supply Chains.

Green Technology Opportunities Across Key ASEAN Markets – 2026 Comparison

| Country | Solar Potential | Wind Potential | Biomass & Green Hydrogen | Key Advantages for GCC Investors |

|---|---|---|---|---|

| Vietnam | Very High (fastest recent growth) | High (onshore & offshore) | Growing interest in green hydrogen | Strong policy support, experienced local partners, competitive PPAs |

| Indonesia | High (archipelagic potential) | Moderate to High | Very High (biomass from palm oil & agriculture) | Large domestic market, resource diversity, green financing opportunities |

| Malaysia & Thailand | High | Moderate | High biomass + emerging hydrogen | Mature infrastructure, strong industrial base, corporate PPA demand |

| Philippines | High | High (offshore potential) | Moderate to High | Growing energy demand, policy reforms, project pipeline expansion |

This comparison highlights the diverse entry points available across ASEAN for GCC investors and technology providers seeking exposure to the region’s green technology growth story.

Policy Frameworks and Investment Climate

ASEAN member states have introduced a range of policy tools to accelerate renewable energy deployment, including:

- Renewable portfolio standards and renewable energy targets

- Feed-in tariffs, auction mechanisms, and corporate power purchase agreements

- Tax incentives, import duty exemptions, and accelerated depreciation

- Green financing facilities and international climate funds

The investment climate continues to improve as governments address grid integration challenges, streamline permitting processes, and enhance transparency in procurement. International investors benefit from growing familiarity with ASEAN markets and increasing availability of project finance tailored to renewable energy characteristics.

How GCC Businesses Can Capitalize on ASEAN Green Technologies in 2026

The Gulf Cooperation Council (GCC) countries are accelerating their own energy diversification strategies while seeking diversified investment opportunities and technology partnerships abroad. ASEAN’s rapid progress in green technologies presents a compelling strategic fit for GCC investors, project developers, technology providers, and industrial players looking to expand their footprint in high-growth Asian markets.

With abundant capital, strong project finance expertise, and growing demand for ESG-compliant investments, GCC entities are well-positioned to participate in ASEAN’s green energy transition. Key opportunities include:

- Project Development & Investment: Participating in utility-scale solar, offshore wind, and green hydrogen initiatives through joint ventures or direct equity investment. Many ASEAN projects seek experienced partners with access to long-term capital and Islamic financing structures.

- Technology Supply & EPC Services: Exporting high-quality solar components, inverters, mounting systems, energy storage solutions, and grid integration technologies. GCC companies with established manufacturing or trading capabilities can leverage ASEAN’s demand surge.

- Green Logistics & Sustainable Supply Chains: Investing in or partnering for green hydrogen applications in maritime and heavy transport, as well as sustainable aviation fuel and biofuel projects that align with GCC’s expertise in energy transition.

- Green Finance & Carbon Markets: Providing Shariah-compliant green financing, sukuk structures, and carbon credit mechanisms to support ASEAN projects while meeting international ESG reporting standards.

Successful GCC players in ASEAN typically combine local partnerships with deep technical and financial expertise. Early movers are focusing on countries with clear policy frameworks and strong resource potential, such as Vietnam for solar, Indonesia for biomass and geothermal, and Malaysia/Thailand for emerging green hydrogen and offshore wind.

By aligning with ASEAN’s sustainability goals and leveraging their own energy transition experience, GCC businesses can achieve attractive risk-adjusted returns while contributing to regional decarbonization and strengthening South-South economic ties.

Risk Management and Compliance Considerations for Renewable Energy Investors

Successful renewable energy investment in ASEAN requires disciplined risk management across multiple dimensions:

- Political and regulatory risk assessment

- Grid connection and offtake security analysis

- Environmental and social impact management

- Currency and financing risk mitigation

- Technology performance and long-term asset management

Investors should implement robust due diligence processes, engage experienced local partners, and structure projects with clear contractual safeguards. Transparent reporting and alignment with international ESG standards enhance access to green finance and strengthen stakeholder relationships.

Renewable Energy Investors

Investing in ASEAN green technologies requires a disciplined, multi-layered risk management approach. Key areas include:

- Regulatory & Policy Risk: Changes in feed-in tariffs, auction rules, local content requirements, and grid connection policies.

- Grid Integration & Offtake Risk: Ensuring reliable power purchase agreements and addressing intermittency challenges through storage and hybrid solutions.

- Environmental, Social & Governance (ESG) Compliance: Meeting international standards for environmental impact assessments, community engagement, and transparent reporting.

- Currency & Financing Risk: Managing foreign exchange exposure and structuring projects with appropriate blend of development finance, commercial lending, and green bonds.

- Technology & Operational Risk: Selecting proven technologies with strong performance warranties and implementing robust operations and maintenance programs.

Successful investors conduct comprehensive due diligence, engage experienced local legal and technical advisors, and structure projects with clear contractual protections. Alignment with global ESG frameworks not only reduces risk but also improves access to competitive financing and enhances reputation with stakeholders.

Practical Investment Roadmap for Renewable Energy Projects in ASEAN

Investors can follow a structured approach to renewable energy project development in ASEAN:

Phase 1: Market and Site Selection

Identify priority countries and technologies based on resource availability, policy support, and grid conditions. Conduct detailed site assessments and resource measurements.

Phase 2: Project Structuring and Due Diligence

Develop bankable project structures, conduct comprehensive technical, financial, legal, and environmental due diligence, and secure necessary permits and approvals.

Phase 3: Financing and Contracting

Structure financing packages that may include development finance, commercial banks, export credit agencies, and green bonds. Negotiate robust power purchase agreements and EPC contracts.

Phase 4: Construction, Commissioning, and Operations

Execute projects with strong health, safety, and environmental management. Implement effective operations and maintenance programs to maximize long-term performance.

90-Day Renewable Energy Opportunity Assessment Checklist

Days 1–15: Strategic Mapping

- Define investment objectives and risk appetite

- Map priority ASEAN countries and technologies

- Assemble cross-functional investment team

Days 16–45: Preliminary Analysis

- Conduct high-level resource and policy assessments

- Identify potential project sites and partners

- Perform initial financial modeling and risk screening

Days 46–75: Detailed Evaluation

- Engage local advisors and conduct site visits

- Develop detailed project structures and compliance frameworks

- Prepare initial financing concepts

Days 76–90: Decision and Preparation

- Complete feasibility studies and due diligence

- Secure preliminary approvals and offtake indications

- Prepare detailed investment memorandum and next-step action plan

Conclusion: ASEAN as a Premier Destination for Green Energy Investment

Southeast Asia’s renewable energy transition represents one of the most compelling investment stories in the global clean energy sector. Driven by strong policy support, improving economics, and rising demand for sustainable solutions, the region offers diverse opportunities across solar, wind, hydropower, biomass, and emerging green hydrogen technologies.

For international investors and technology providers, success in ASEAN requires a balanced approach that combines technical excellence, local market understanding, robust risk management, and unwavering commitment to responsible business practices. Those who engage with discipline, transparency, and long-term vision will be well positioned to capture both commercial returns and meaningful environmental impact.

The continued development of renewable energy in ASEAN will play a vital role in the region’s sustainable economic growth and its contribution to global climate objectives. Companies and investors that align their strategies with this transition today will help shape a cleaner, more resilient energy future for Southeast Asia and beyond.

Platforms purpose-built for regulated sustainable investment provide the operational infrastructure necessary to identify, develop, and manage renewable energy projects efficiently and compliantly. Entities seeking to strengthen their participation in ASEAN’s green energy transition are encouraged to evaluate integrated solutions that combine investment expertise with full regulatory alignment.

Request a Confidential ASEAN Renewable Energy Investment Assessment