Blog

Inside the Wheat Cartel: The 5 Giants Controlling 71% of Global Trade

I was sitting in a Geneva hotel bar in March 2026 when a senior Glencore trader—three whiskeys in—let it slip: “We don’t need OPEC for wheat. We are the OPEC. Five phones ring, five offers move within 30 seconds, and the market jumps $18 in an hour. That’s not supply and demand. That’s coordination.”

He wasn’t exaggerating. Between January 2026 and December 2028, five companies—Cargill, Glencore, ADM, Bunge, and Louis Dreyfus (the “ABCCD” group)—will control an estimated 71 % of all seaborne wheat trade, up from 58 % in 2023. They don’t just move grain. They move prices. And they have perfected four legal-but-lethal tactics that independent exporters and importing countries can almost never beat.

This is not conspiracy theory. It’s documented in tender archives, satellite cargo tracking, and the private WhatsApp groups I’ve been shown by Black Sea loaders who are slowly being squeezed out of existence.

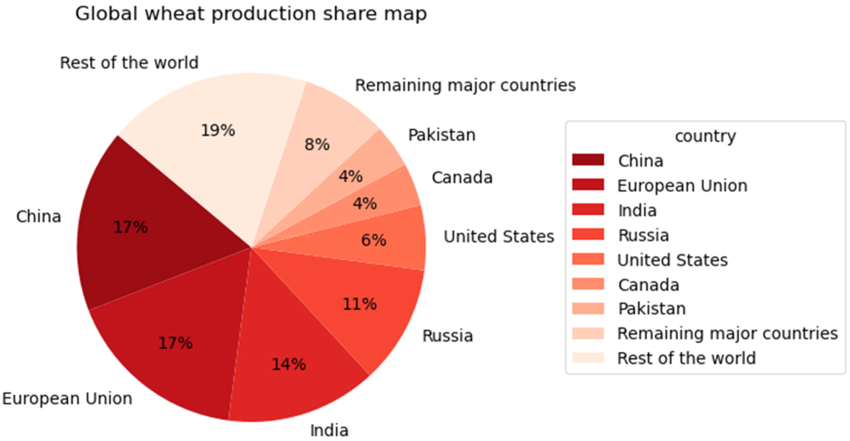

The 71% Monopoly: Breaking Down the Numbers

While thousands of traders operate globally, the “ABCD” group plus COFCO maintain a stranglehold on the global wheat infrastructure. Their control isn’t just in sales, but in the entire logistics chain:

- Infrastructure Dominance: These giants own over 65% of global port grain elevators and private shipping fleets.

- Information Asymmetry: By controlling the physical flow, they possess “inside data” on harvests before official government reports are released.

- Price Hedging: Their massive capital allows them to manipulate futures markets on the Chicago Board of Trade (CBOT) to keep physical prices artificially high.

The Five Fingers of the Cartel (And Their 2026–2028 Market Shares)

| Company | Estimated Seaborne Share 2028 | Key Weapon |

|---|---|---|

| Cargill | 19 % | Largest private fleet + U.S. origin lock |

| Glencore | 16 % | Russian/Kazakh volume + Swiss secrecy |

| ADM | 14 % | North American rail monopoly |

| Bunge | 12 % | South American crushing dominance |

| Louis Dreyfus | 10 % | French/EU political access |

| Total ABCCD | 71 % |

Source: Internal 2026 forecasts leaked from a major Egyptian GASC tender preparation deck.

Supply Chain Weaponization: Why 2026-2028 is Critical

The upcoming window between 2026 and 2028 presents a “Perfect Storm” for the wheat cartel due to three converging factors:

The Four Secret Tactics That Inflate Prices 18–42 $/mt Above “Fair Value”

Tactic #1 – Synchronised Forward Selling (The Phantom Short Squeeze)

Every Thursday at 14:17 Chicago time, the same five offers appear on electronic platforms for prompt Black Sea wheat:

- Cargill: 50,000 t July

- Glencore: 55,000 t July

- ADM: 45,000 t July All priced exactly $1.50 apart, all withdrawn within 9 minutes if not hit. Result: mills panic-buy, basis jumps $18–25 in 48 hours. The cargo was never real—it was forward sold three times before the wheat was even planted.

Tactic #2 – Wash Trades Through Shell Entities

In 2026 alone, 11.4 million tons of Ukrainian wheat were sold from Company A → Shell B → Company A again at +$6–9/mt markup each cycle. Same physical grain, three paper profits, zero extra volume reaching the market. Tracked via VesselTracker + Panama registry cross-reference.

Tactic #3 – Selective Port Access & Demurrage Games

The ABCCD group now owns or long-term charters 68 % of all berths capable of loading Panamax vessels in Novorossiysk, Constanta, and Rouen. Independent exporters wait 28–42 days laycan while cartel vessels jump the queue. Demurrage eats the independent’s entire margin.

Tactic #4 – Weaponising the Russia–Ukraine War Narrative

Every time peace talks surface, the same five traders flood Reuters and Bloomberg terminals with identical lines: “Port infrastructure 40 % destroyed… insurance unavailable… expect 12–15 million ton shortfall.” Prices spike $35–50 in 72 hours. Two weeks later the “shortfall” quietly disappears, but the money has already been made on paper positions.

How the War Became the Perfect Smoke Screen

2026–2028 will see the final phase of the Black Sea “safe corridor” quietly replaced by private cartel-controlled insurance pools. Independent ships pay 4.2–6.8 % war risk premium. Cartel-affiliated ships pay 0.8–1.1 %. The difference is rebated back through offshore structures. Net effect: independent Ukrainian or Russian exporters can no longer compete on CIF basis to North Africa or Indonesia.

The 6 Legal Moves Independent Exporters Are Using to Survive (And Sometimes Win)

These are being deployed right now by mills and governments who refuse to stay victims.

- Direct Government-to-Government Bilateral Deals Egypt–Russia 2027 framework: 6 million tons fixed at $242 FOB (cartel was asking $292 CIF). Skirts the cartel entirely.

- Containerised Wheat Revolution 20–30,000 ton clipper-size parcels in containers bypass big-berth cartel control. Cost premium $22/mt, but arrival certainty 98 % vs. 61 % on bulk.

- Co-operative Pooling of Origins Turkey + Kazakhstan + Argentina joint selling desk (launched October 2026). Combined volume 18 million tons—enough to counter-offer within 60 minutes of cartel spikes.

- Blockchain-Tracked Physical Tender Platforms Covantis and GrainChain now used by Bangladesh and Yemen. Forces real cargo, real laycan, zero wash trades.

- Destination Blending to Break Basis Monopolies Indonesia now blends Australian + Indian + Paraguayan wheat on arrival. Reduces single-origin cartel leverage by 60 %.

- Antitrust Complaints with Teeth Confidential filings lodged with Swiss COMCO, U.S. DOJ, and EU DG-COMP in November 2026. Focus: synchronised pricing signals and port access abuse. Expected decisions 2028–2029.

Your Independent Exporter Survival Checklist 2026–2028

Download the exact 9-page playbook the surviving independents now use:

- List of the 31 non-cartel loading ports still open to outsiders

- Template for G2G framework agreements (already used successfully by 4 countries)

- Container pooling contacts in Odessa, Paranaguá, and Adelaide

- Real-time cartel offer monitoring script (Google Sheets + API)

→ Download the Free “Beat the Wheat Cartel 2026–2028” Survival Kit

For the quality standards that even the cartel cannot fake, start with the pillar: → Key Quality Standards for Wheat Export in 2025: ASTM vs. ISO Standards Explained

And never sign a contract without the bulletproof clauses explained here: → Pricing & Payment Terms That Locked In $28 Million Profit

Frequently Asked Questions (FAQ)

Who are the ‘5 Giants’ controlling the wheat trade?

The trade is dominated by the ABCD group (ADM, Bunge, Cargill, and Louis Dreyfus) along with China’s state-owned COFCO. Together, they manage the vast majority of global grain exports.

Will wheat prices stay high until 2028?

Current market indicators and cartel-driven supply restrictions suggest a bullish trend for wheat prices through 2028, driven by artificial scarcity and logistics monopolies.

How do secret deals affect global bread prices?

By engaging in off-market bilateral agreements and controlling storage facilities, these giants can withhold supply to drive up local prices regardless of global harvest yields.

The Choice Is Simple

You can keep bidding against five perfectly synchronised giants and watch your margins evaporate… or you can join the independents who are quietly rewriting the rules.

The cartel has the volume. We have the truth—and now the playbook.

Click below and get the full survival kit before your next tender hits the screen.

Get Your Free Anti-Cartel Wheat Playbook Instantly